Tax Treatment of Change to LIFO

For tax purposes, the IRS allows all taxpayers to use LIFO method, and establishing preferability regarding the use of LIFO is not required. The tax requirements incident with and subsequent to a LIFO election are as follows:

- LIFO must be applied as a cutoff change, meaning it’s to be applied prospectively beginning in the year of change (no Sec. §481(A) or prior period adjustments are permitted for the change to LIFO method)

- Financial reports or statements must present the face of the income statement & balance sheet on a LIFO basis in the first period that inventory & income is determined on a LIFO basis on the tax return (non-LIFO disclosures & supplemental schedules presenting income/inventory on a non-LIFO basis can be used on financial reports/statements)

- Must attach IRS Form 970 Application to Use LIFO Inventory Method to tax return in the first year that inventory is valued & income is determined on a LIFO basis for tax purposes (amended return can be used to elect LIFO as long as it’s filed within 12 months of the date original return was filed & Form 970 is attached to amended return)

- Must value beginning & closing inventories at cost in the year of LIFO adoption

- Any non-LIFO inventory reserves or write-downs to below cost that were included in the computation of the inventory value and determination of income on the tax return prior to the LIFO election must be ratably recaptured into income over a three year period beginning in the LIFO election (no recapture is required if the inventory reserves or write-downs below cost were accounted for as a Schedule M adjustment on the tax return prior to adopting LIFO)

- LIFO inventories can be valued at the lower of cost or market for financial reporting purposes, but must be valued at cost for tax; accordingly, if reserves or write-downs below cost are maintained for financial reporting purposes incident & subsequent to the LIFO election, a Schedule M adjustment must be recorded on the tax return to account for the difference between the financial reporting & tax Current-year cost.

Financial Reporting (GAAP) Treatment of Change to LIFO

All changes in accounting principle require entities to justify the use of an allowable alternative accounting principle on the basis that it is preferable. Accordingly, companies issuing GAAP financial reports who make a change to the LIFO method are required to establish it as a preferable method.

GAAP requires for accounting method changes to be applied retrospectively unless it’s impracticable to do so. With LIFO, nearly all companies apply LIFO prospectively on the justification that it’d be impracticable to apply it retrospectively. To our knowledge, the most recent example of a publicly-traded company changing to the LIFO method is United Natural Foods in 2019 (Ticker: UNFI). Their preferability statement and justification for the prospective application provided within their 10-K inventory disclosure is provided below (see UNFI’s 10K containing LIFO change disclosures):

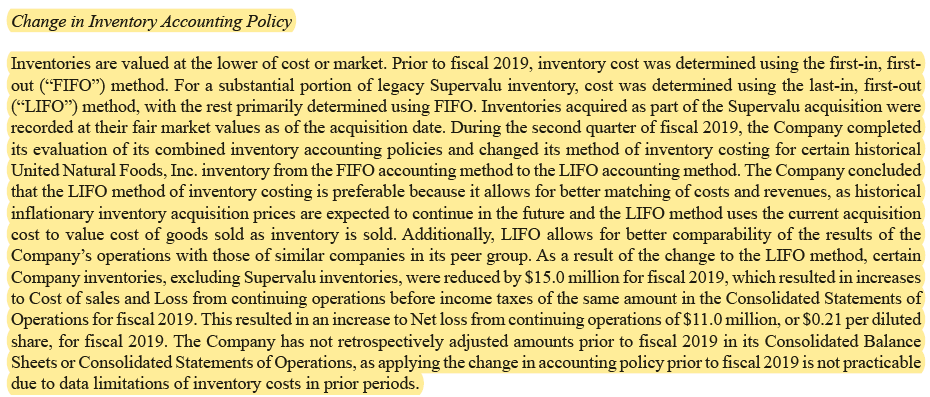

Figure 1. United Natural Foods 2019 Year End 10-K Disclosure Regarding Change to LIFO Method

As seen above, UNFI changed from the FIFO method to the LIFO method for certain inventories for the 2019 year end. When this change was made, it was applied prospectively because doing so would not have been practicable, “due to data limitations of inventory costs in prior periods.”

The impracticability exception is almost always applied for justifying applying the change to the LIFO method prospectively. Although there is no formal financial reporting authoritative guidance that provides an exception to prospectively applying the change to the LIFO method, the UNFI change to LIFO is a case in point to this fact. Computerized accounting information systems & perpetual inventory records have been commonplace within large companies for the last 2 – 3 decades. Knowing this, it’s safe to assume that UNFI likely had at least 5 – 10 years of the inventory accounting records required to retrospectively apply LIFO.

One fact that favors the prospective application of the LIFO method for financial reporting purposes is that the IRS requires taxpayers to do so (no exceptions exist regarding the prospective application of LIFO for tax purposes). Since this is the case, the retrospective treatment for the change to the LIFO method would result in different book vs. tax base years and for separate calculations to be performed. Because of this, companies and CPA firms are usually motivated to also apply LIFO prospectively for financial reporting purposes as it allows for book & tax LIFO conformity and requires for only a single LIFO calculation to be made.

Establishing LIFO as a Preferable Method for Financial Reporting

No authoritative body has specified criteria for determining the preferability of the LIFO method over all non-LIFO methods. The Securities and Exchange Commission’s Codification of Staff Accounting Bulletins provided interpretative response for dealing for such situations, which is provided below (see SEC Codification of Staff Accounting Bulletins – Topic 6: Interpretations of Accounting Series Releases and Financial Reporting Releases, Section G(2)(b)(1)).

Question 1: For some alternative accounting principles, authoritative bodies have specified when one alternative is preferable to another. However, for other alternative accounting principles, no authoritative body has specified criteria for determining the preferability of one alternative over another. In such situations, how should preferability be determined?

Interpretive Response: In such cases, where objective criteria for determining the preferability among alternative accounting principles have not been established by authoritative bodies, the determination of preferability should be based on the particular circumstances described by and discussed with the registrant. In addition, the independent accountant should consider other significant information of which he is aware.

Question 2: Management may offer, as justification for a change in accounting principle, circumstances such as: their expectation as to the effect of general economic trends on their business (e.g., the impact of inflation), their expectation regarding expanding consumer demand for the company’s products, or plans for change in marketing methods. Are these circumstances which enter into the determination of preferability?

Interpretive Response: Yes. Those circumstances are examples of business judgment and planning and should be evaluated in determining preferability. In the case of changes for which objective criteria for determining preferability have not been established by authoritative bodies, business judgment and business planning often are major considerations in determining that the change is to a preferable method because the change results in improved financial reporting.

Question 3: What responsibility does the independent accountant have for evaluating the business judgment and business planning of the registrant?

Interpretive Response: Business judgment and business planning are within the province of the registrant. Thus, the independent accountant may accept the registrant’s business judgment and business planning and express reliance thereon in his letter. However, if either the plans or judgment appear to be unreasonable to the independent accountant, he should not accept them as justification. For example, an independent accountant should not accept a registrant’s plans for a major expansion if he believes the registrant does not have the means of obtaining the funds necessary for the expansion program.

Inflation is the primary component in determining LIFO’s financial reporting impact and tax benefits. Accordingly, it’s safe to assume that establishing LIFO as a preferable method should primarily revolve around measuring past, present & expected future inflation, and quantifying LIFO’s effect on income and tax liability.

As a firm dedicated exclusively to LIFO, we developed a grading system and scoring criteria for establishing whether or not LIFO is a preferable method, and for also determining the appropriate LIFO election timing. Our grading system and scoring criteria is outlined below:

- Scoring: The following inflation criterion are measured to establish LIFO’s preferability & determine the LIFO election timing

- 20 Year Average Annual Inflation Rate: The 3/5/10/20 year average annual inflation rates are measured by assigning Bureau of Labor Statistics Consumer/Producer Price Index categories (BLS CPI/PPI) to the current period’s product mix and performing LIFO calculations for each of the past 20 years

- 20 Year Average Inflation Frequency: Inflation frequency is measured using the results of the 20 year pro forma IPIC LIFO calculation and is used to determine how often LIFO has created a tax benefit historically

- Election Year Inflation Multiplier: Measured by dividing the current year inflation rate by the 20 year average annual inflation rate

- Criteria: The following criterion must be met for LIFO to be established as a preferable method:

- Preferability Criteria

- The 20 year average annual inflation rate calculated from each of the past 20 year’s IPIC LIFO calculations must be greater than or equal to 1%

- The 20 year inflation frequency rate must be greater than or equal to 50% (10 or more of 20 years)

- Current Year LIFO Election Criteria

- All preferability criteria listed above must be met

- Election year inflation multiplier is greater than or equal to 1 (current year inflation rate is greater than or equal to the 20 year average annual inflation rate)

- Preferability Criteria

LIFOPro uses the above grading system as the basis for providing complimentary LIFO election benefit analysis and preparing a PDF report containing comprehensive documentation of our findings and recommendations. This allows companies and CPA firms to estimate LIFO’s present and long-term financial reporting and tax impacts, and understand both the risks and rewards associated with the use of the LIFO method. Learn more here: LIFO Election Benefit Analysis